The Economics of Building With AI: What the Numbers Actually Show

AI collapsed the cost of building. It didn’t collapse the cost of distribution. Here’s what that means for revenue teams.

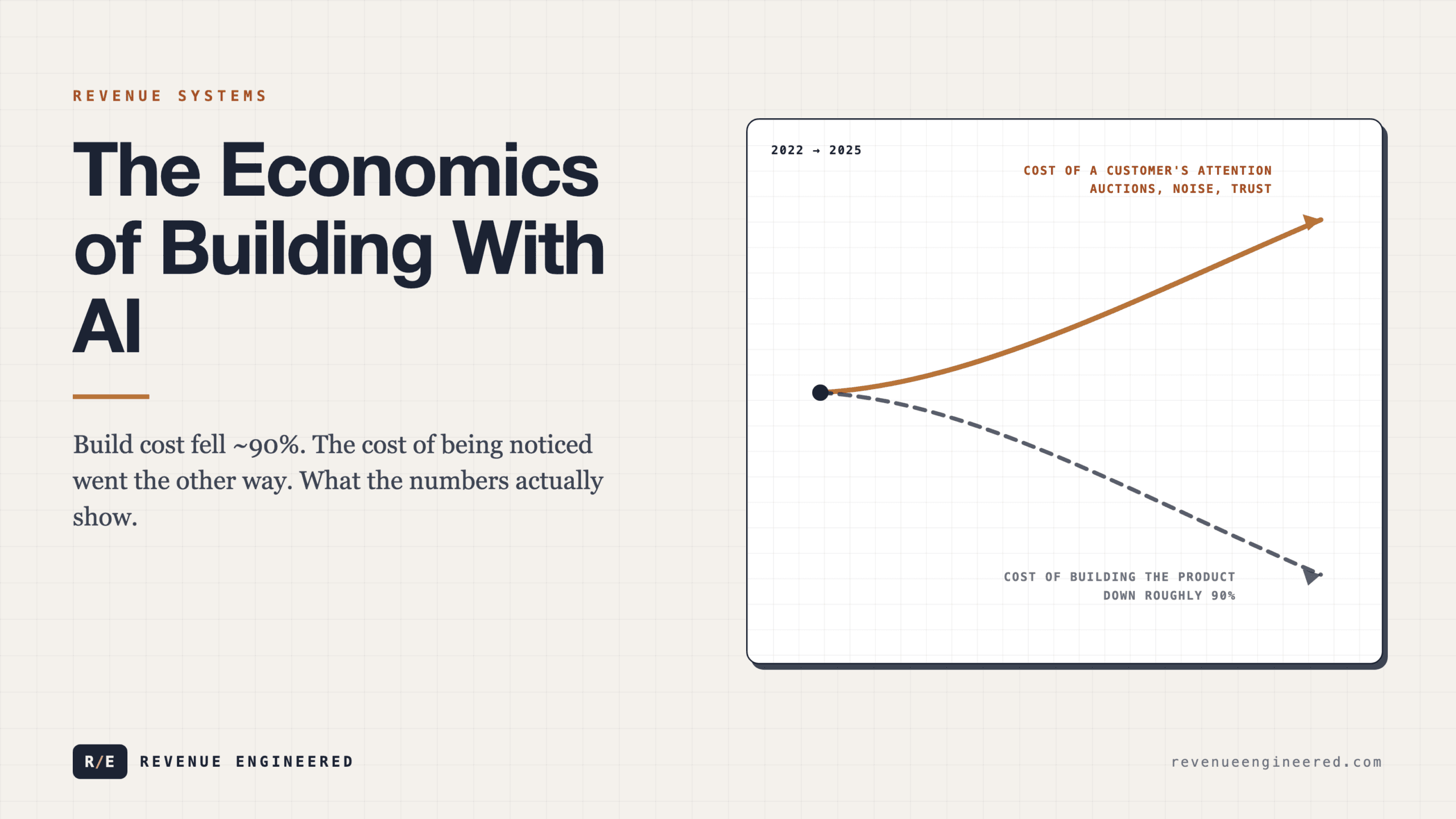

The cost of building a software product dropped by roughly 90% between 2022 and 2025. That is a measurable fact visible in the financial statements of thousands of bootstrapped companies operating right now, not a projection or a thesis statement. What has not dropped by anything close to 90% is the cost of getting that product in front of the right buyer at the right moment. This asymmetry between build cost and distribution cost is the defining economic reality of the current era, and most teams are drawing exactly the wrong conclusions from it.

The popular narrative goes something like this: AI makes everything cheaper, therefore startups need less money, therefore more people can start companies, therefore we will see an explosion of new products competing in every category. That narrative is directionally correct and operationally useless. It tells you nothing about where to allocate resources, how to structure a team, or which costs actually determine whether the business survives past month eighteen. The numbers tell a different story, and that story has specific implications for anyone building a revenue function today.

What $456,000 in savings actually looks like

AI compresses operating cost, not demand cost..

A solo operator running a six-figure monthly business recently documented their full cost audit. They went through their stack line by line, asking three questions about each subscription: can this be replaced with something cheaper, can it be built internally, or can it be eliminated entirely. The answer was yes for roughly 80% of their recurring tools. The result was $456,000 per year in eliminated operating costs. Profit margins moved from 67% to 87% in a single month.

The composition of those savings matters more than the headline number. The largest categories were not the obvious ones. NSFW image detection went from a $2,000/month third-party service to an internally built solution running at $50/month. Daily email sends were consolidated into weekly digests, cutting platform costs by 90%. Human content moderation and copywriting were replaced with AI at roughly a 1,000x cost reduction. Customer triage followed the same pattern. None of these were moon-shot engineering projects. They were methodical substitutions, executed over a few weeks, by a single person with access to modern AI tooling.

This pattern is now repeating across the entire bootstrapped economy. The total addressable cost that AI can compress for a small software business is somewhere between $200,000 and $600,000 per year, depending on the category. That compression changes the math on everything downstream. It changes when a company reaches profitability. It changes how many customers are required to sustain the operation. It changes the entire calculus around outside funding.

The distribution cost problem nobody solved

Product got cheaper. Attention did not..

Here is where the narrative breaks. AI collapsed build costs. It collapsed operational costs. It collapsed the cost of content production, customer support, and basic engineering. It did not collapse the cost of acquiring a customer who is willing to pay money every month.

Distribution remains expensive and fundamentally human. Cold outreach still requires understanding the buyer’s context. SEO still requires months of compounding before it produces meaningful traffic. Paid acquisition still operates on auction dynamics where the price rises as more competitors enter. Brand building still takes years of consistent presence. Referral networks still depend on trust that cannot be manufactured by a language model.

The gap between build cost and distribution cost is widening, not narrowing. As AI makes it cheaper to create products, more products enter every category. More products means more noise. More noise means distribution becomes harder and more expensive per customer acquired. The irony is that the same technology that lowered the barrier to building raised the barrier to being noticed. A market flooded with AI-generated SaaS products does not reward the best product. It rewards the best distribution.

The founders and revenue leaders who understand this asymmetry are making very different resource allocation decisions than the ones who don’t. They are spending less on engineering and operations — because AI compressed those costs — and redirecting that budget toward distribution. They are hiring for GTM before they hire for product. They are building audiences before they build features. They are treating distribution as the scarce resource and product as the commodity, which is the inverse of how most technology companies have operated for the past twenty years.

This inversion is a structural shift in how technology businesses create value, not a passing trend. The product is no longer the moat. Distribution is the moat. The product is the thing inside the moat. And the teams that figure this out first will have a compounding advantage that becomes very difficult to overcome.

Two people producing the output of ten

Two people can cover the old ten-person surface area..

The most operationally interesting development in the current environment is the emergence of two-person teams generating revenue that previously required eight to twelve people. These are real businesses, running real revenue, with real customers, not hypothetical constructs. They look nothing like the organizational charts that dominated the previous decade.

The typical profile: one person owns product and engineering. One person owns distribution and revenue. Between them, they cover backend code, frontend code, testing, UI, UX, onboarding flows, server infrastructure, customer support, pricing, payment processing, email marketing, social media, SEO, competitor monitoring, growth strategy, and ad management. They do this at $100,000 per month in revenue with operating costs under $1,500.

The math on that structure is worth sitting with. A $100K/month business at 85% margins generates roughly $85,000 in monthly profit. After taxes, approximately $68,000 per month goes to the two operators. Split evenly, each person earns more than a VP-level salary at a Series B startup while maintaining full ownership, full control, and zero dilution.

The reason this works now and did not work five years ago is that AI eliminated the long tail of operational tasks that used to require specialized hires. You no longer need a dedicated customer support agent when AI handles triage. You no longer need a junior developer for bug fixes and CSS when AI writes and tests that code. You no longer need a content writer when AI produces first drafts that a human editor refines in minutes. Each of these eliminations is individually small. Collectively, they remove five to eight full-time roles from the org chart.

What makes these teams structurally durable is that the operating cost floor stays low regardless of revenue growth. A ten-person company scaling from $100K to $500K per month in revenue needs to hire proportionally. A two-person company making the same jump does not. Their infrastructure scales with the software, not with headcount. This means the marginal economics improve with every dollar of revenue, which is the opposite of what happens in traditional team structures where each new revenue milestone triggers a hiring round that consumes most of the new margin.

Recurring revenue as structural defense

The cost compression story gets dangerous when it combines with the wrong revenue model. A business that sells a one-time product and uses AI to lower its build costs has reduced its expenses but not changed its fundamental vulnerability. It still needs to acquire 100 or more new customers every single month just to maintain revenue. Not to grow. To survive. Every month is a cold start. Every month the acquisition pressure resets to zero.

This is the failure mode that shows up repeatedly in the field data. A founder builds something useful. People buy it. Revenue reaches $3,000 or $5,000 per month. It looks like a success story from the outside. But because there is no recurring component, the founder spends all their time on acquisition. They cannot invest in the product because every hour not spent on new customer acquisition feels like lost revenue. They work sixty hours, then eighty, then every waking moment. Health deteriorates. Relationships strain. The business was technically profitable the entire time. The operator’s body broke first.

The structural fix is recurring revenue from day one. Subscriptions. Memberships. Retainers. Monthly billing that locks in 80% or more of this month’s revenue before the month starts. When that base exists, the psychology of running the business changes completely. Decisions improve because they are made from stability, not desperation. Growth compounds because each new customer adds to the base rather than replacing a churned one. The operator can actually take a vacation without the revenue dropping to zero.

The AI cost compression makes this even more powerful. When your operating costs are $1,500 per month and your recurring revenue is $60,000 per month, you are running at margins that no venture-backed company can match. You have more cash flow per employee than most public SaaS companies. And that cash flow compounds in a way that venture capital, by design, does not.

The VC playbook inverted

The traditional venture capital model optimizes for a single event: the exit. Everything before the exit is cost. The exit is the payoff. If the exit does not happen, the entire exercise was wealth destruction for everyone except the employees who collected a salary along the way.

AI-era economics make a different playbook not just viable but mathematically superior for most founders. Run a business at 85% margins. Invest 70% of after-tax profit into broad market index funds. At historical average returns of 11% annually, a $60,000/month business produces $100 million in investment portfolio value over 30 years. No exit required. No board approval needed. No dilution at any stage.

This is a pure financial argument, not a lifestyle business argument. The expected value of the bootstrapped compounding path exceeds the expected value of the venture path for the vast majority of founders, because the venture path has a 90%+ failure rate while the compounding path is mathematically guaranteed if revenue remains stable and investments remain consistent.

The competitive dynamics are shifting accordingly. A venture-backed company burning $200,000 per month on a sales team before signing its first customer is now competing against a two-person operation with near-zero overhead that can undercut on price and move faster on product while surviving indefinitely without external capital. The funded company needs to win fast or die. The bootstrapped company just needs to not quit. Over a long enough timeline, persistence beats speed in almost every market that is not winner-take-all.

The teams that internalize this are structuring their businesses differently. They use AI to stay at two people and route the surplus into investments, rather than raising seed rounds to hire engineering teams. They optimize for margin and cash flow to feed the compounding machine, not ARR growth to attract Series A investors. They build to own, not to sell.

What this means for team structure

The practical implications for anyone building or leading a revenue function are specific. First, the ratio of GTM to engineering spend should invert. If AI reduces your engineering costs by 70%, that 70% should flow to distribution, not to the bottom line. The companies that pocket the savings and keep their distribution spend flat will be outcompeted by the ones that reinvest it into customer acquisition.

Second, the hiring profile changes. The person who matters most on a two-person team is the one who can do product and distribution simultaneously, not the best engineer. The ability to write code, understand the customer, craft a message, and close a deal in the same day now beats deep specialization in any single function. Generalists beat specialists in small-team environments where AI handles the specialist work.

Third, the financial model changes. Monthly operating costs below $1,500. Recurring revenue as the only acceptable model. Margins above 80%. Investment rate above 70% of after-tax profit. Hours tracked and capped at 50 per week. These are the observed characteristics of the two-person teams producing the best risk-adjusted financial outcomes in the current environment, not aspirational targets.

The economics of building with AI are clear. Build costs went to near zero. Distribution costs stayed where they were. The winners will be the teams that reallocate accordingly and let the compounding do what compounding does.

Enjoying this essay?

Written by

Elom

GTM, growth, and revenue systems operator with 12 years across Fortune 500s, fintech, and B2B startups. Building at the intersection of AI, data, demand, and revenue.

Get the next deep-dive in your inbox

Essays on demand creation, GTM, growth engineering, and revenue systems. Free.