When the AI Agent IS the Business: Lessons from Autonomous Revenue

What happens when you remove humans from the revenue loop entirely

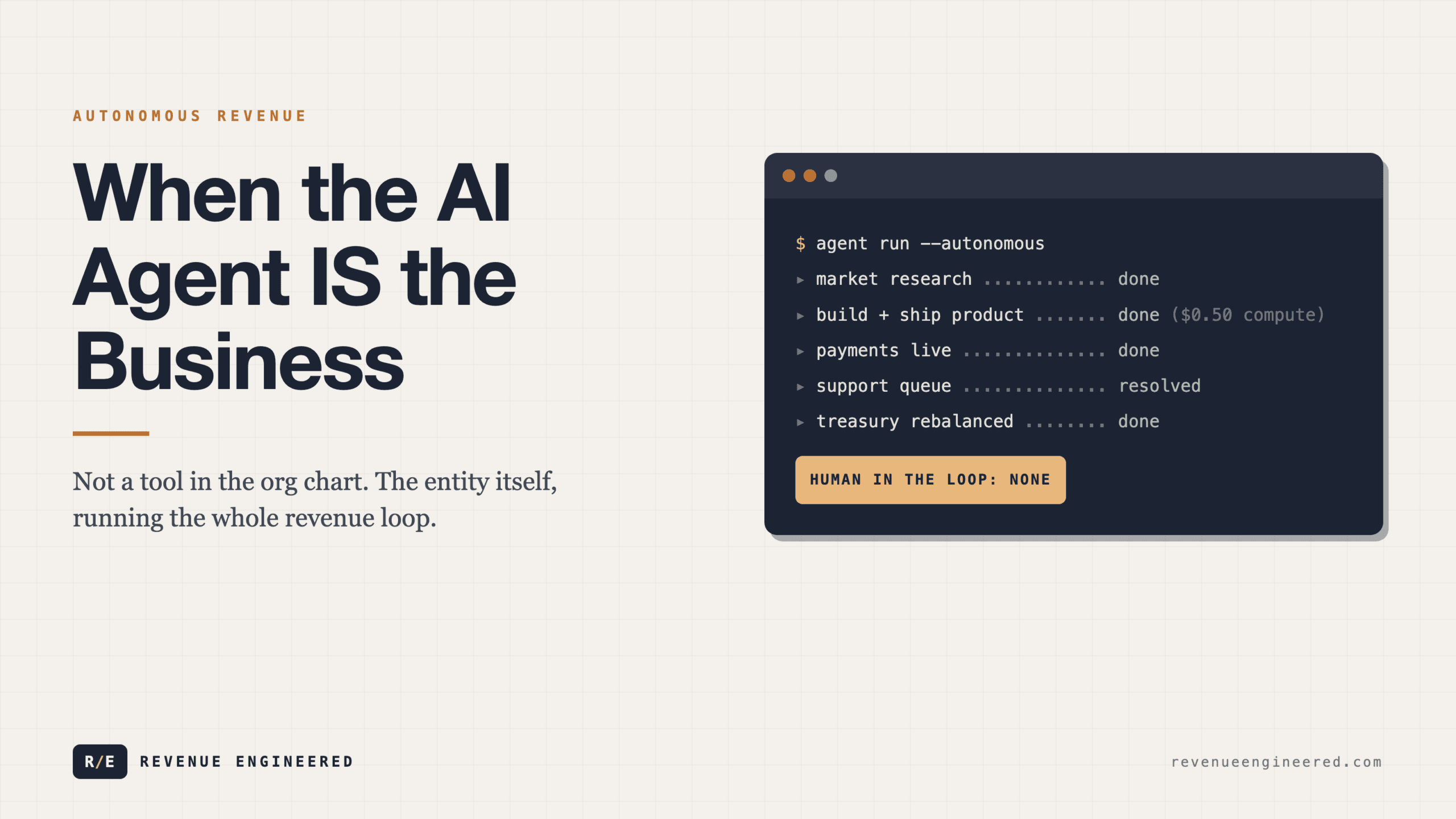

Somewhere in the last year, the conversation shifted. We went from “AI agents can help your business” to “AI agents can run your business” to something nobody quite expected: AI agents that are the business. Not a tool inside the org chart. Not a copilot sitting next to a human operator. The entity itself. An agent that identifies market opportunities, builds products, deploys them, markets them, handles payments, does customer support, and reinvests the proceeds. All without a human touching the revenue loop.

This is not a thought experiment. There are AI agents generating real revenue right now. One agent shipped over 85 apps in a single weekend, got approved by the Apple App Store autonomously, and hit $1,000 in daily revenue within weeks of launch. Another agent earns five figures per week through a combination of product sales, marketplace commissions, and service fees. The factory that produces these outputs runs 24/7. It evaluates itself every 60 minutes. It researches markets, scores opportunities, spawns sub-agents to build in parallel, tests its own output, and deploys finished products to production environments.

If your mental model of “AI in business” is still “a chatbot on your website,” you are behind by about three paradigm shifts.

The evolution nobody planned for

evolution nobody planned for reframed as system design.

There is a progression here worth mapping clearly, because where you are on this spectrum determines what you should be worried about and what you should be building toward.

Stage 1: Human business. A person does every job. They research, build, sell, support, invoice, and collect. This is how businesses worked for thousands of years. Every dollar of revenue requires human labor to produce. The constraint is time.

Stage 2: Human + AI tools. The business is still human-operated, but AI handles discrete tasks. A founder uses ChatGPT to draft marketing copy, Cursor to write code faster, an AI tool to generate ad creatives. The human is still in every decision loop. AI is a productivity multiplier, not a decision-maker. Most companies in 2026 are here. The constraint is that every AI tool still needs a human to invoke it, review its output, and decide what to do next.

Stage 3: Human-directed AI agents. The human sets goals and guardrails. The agent figures out how to achieve them. A growth operator tells an agent “research these 50 accounts and identify the best entry point for each one.” The agent selects its own tools, decides what information matters, and delivers a synthesis. The human reviews the output and acts on it. This is where the most advanced GTM teams operate today. The constraint is that humans are still the bottleneck on throughput. An agent can produce research 10x faster than a human, but if a human still needs to approve every action, you have only shifted the bottleneck, not removed it.

Stage 4: Autonomous AI business. The agent receives a high-level objective (“reach $1 million in revenue as quickly as possible with as much recurring revenue as possible”) and operates independently to achieve it. It identifies markets, builds products, launches them, markets them, processes payments, handles support, and iterates based on results. Human involvement is limited to setting the objective and occasionally intervening when something breaks. This is where a small but growing number of experiments are operating right now.

The jump from Stage 3 to Stage 4 looks small on paper. In practice, it requires a fundamentally different architecture. In Stage 3, the human is the orchestrator. In Stage 4, the agent is the orchestrator, and the human is an exception handler.

What autonomous revenue actually looks like

The real examples are instructive because they reveal both the potential and the constraints that the hype cycle glosses over.

Consider the autonomous software factory model. An agent runs market research on app categories, scores opportunities by TAM, competition density, and revenue potential. It identifies niches where the manual process costs 10-20 hours and the automated version can be sold for $99. It then spawns teams of sub-agents: builders, testers, security auditors, and deployment agents. Twelve builder agents can produce a complete platform in ten minutes. Four hostile agents then attack it, finding 109 vulnerabilities that get patched before launch.

The cost per completed iOS app: roughly $0.50 in compute.

The margins on a $99 product built for $0.50: 96%+.

The production rate: 15 unique applications built overnight, with plans to scale to hundreds.

This is not hypothetical. These numbers come from publicly documented autonomous agent operations. The agent that produced these results also autonomously submitted apps to the Apple App Store, got approved, and started generating revenue without any direct human involvement in the build-to-revenue pipeline.

The second model is the agent-as-marketplace operator. An agent builds and manages a two-sided marketplace where AI agents buy skills and services from other AI agents. Agent-to-agent payments crossed $2,000 early on, with no human in the loop. The agent handles marketplace operations, customer support emails (including Apple Pay delivery issues and account problems), and even manages its own treasury, deciding how to deploy capital across API costs, developer bounties, and product distribution.

That last part is worth pausing on. An AI agent making capital allocation decisions. Deciding whether to spend its revenue on infrastructure, marketing, or talent. That used to be the exclusive domain of a CFO or a founder. Now it is a prompt.

The economics of near-zero marginal cost

The business model math for autonomous agent businesses is unlike anything in traditional software economics. In SaaS, the marginal cost of serving an additional customer is low but not zero. You still need servers, support staff, account managers, and infrastructure that scales with usage. The revenue-per-employee benchmarks we track in this newsletter ($200K-$300K for traditional SaaS, $3M+ for AI-native companies) assume that employees exist.

An autonomous agent business has a different cost structure entirely. The primary costs are compute (API calls and inference), infrastructure (hosting and deployment), and the initial system design. There is no payroll. There is no office. There are no benefits, no PTO, no management overhead. When the agent is both the builder and the operator, the marginal cost of an additional product or an additional customer approaches the cost of the API calls required to serve them.

One operator described his autonomous agent setup as “a two-person company where one of us doesn’t sleep.” The human handles the 5% of tasks that still require meatspace judgment. The agent handles the other 95%, around the clock, including weekends and holidays. The agent’s first week of operation generated over $41,000 in revenue across product sales and trading fees.

The scaling dynamics are also different. A human business scales linearly at best. Hiring one more rep gets you roughly one more rep’s worth of output. An autonomous agent business scales by spawning more instances. Need to build 15 apps tonight instead of 5? Spin up more sub-agents. Need to handle 10x the support volume? Deploy more support instances. The ceiling is compute budget, not labor supply.

Where it breaks down

Where it breaks down as a maturity path.

The temptation here is to extrapolate these early results into a world where autonomous agents replace every business. That would be wrong, and the reasons why are important to understand.

Quality at the edges. The autonomous factory model works well for products that are well-defined and repeatable. Utility apps, identifier tools (bird ID, mushroom ID, rock ID), simple SaaS products with clear value propositions. These are markets where “80% as good as the best human-built product at 10% of the price” is a winning proposition. But for products that require deep domain expertise, nuanced UX design, or novel problem-solving, the agent-built output is still detectably generic. The gap between “functional app” and “product people love” has not been closed by autonomous agents. It has been narrowed, but the remaining gap is where the hardest value lives.

Brand risk compounds silently. When a human makes a mistake in customer communications, it affects one interaction. When an autonomous agent makes a systematic error in how it handles support tickets, pricing, or product claims, it affects every interaction until someone notices. The failure mode for autonomous businesses is not the spectacular crash. It is the slow accumulation of small errors that erode trust without triggering any alert. One agent documented handling customer support emails for Apple Pay delivery issues, security questions, and account problems. Each of those interactions carries regulatory and reputational exposure that a $0.50 compute cost does not price in.

Regulatory exposure is uncharted. Who is liable when an autonomous agent makes a misleading product claim? When it processes a payment for a product that does not work as described? When it collects user data without proper consent flows? The legal frameworks governing autonomous commercial activity are essentially nonexistent in 2026. Companies experimenting with autonomous agent businesses are operating in a regulatory vacuum. That vacuum will not last. The first major consumer harm incident involving an autonomous agent business will trigger a regulatory response, and nobody knows what that response will look like.

Customer trust requires a principal. People will buy from an AI, up to a point. Simple transactions with clear deliverables, low price points, and easy refund paths work fine. But anything involving ongoing relationships, high-value contracts, or trust-dependent services still requires a human principal that the customer can hold accountable. The experiment of an AI agent explicitly identifying as non-human while selling products is fascinating, but it works because the products are low-cost apps, not enterprise contracts. Selling a $99 permit automation tool is different from selling a $500K consulting engagement. Both require trust, but the kind of trust required is qualitatively different.

What kinds of businesses work as autonomous operations

What kinds of businesses work as autonomous operations translated into operating choices.

The pattern emerging from early experiments suggests a clear boundary between what autonomous agents can run and what they cannot.

Businesses that work well as autonomous operations share specific characteristics: high volume, low unit price, standardized deliverables, short customer relationships, and clear success criteria. Mobile apps. Digital products. Content generation. Data processing services. Marketplace matching. Automated research reports. These are businesses where the customer cares about the output, not the process. Nobody cares that their fish identification app was built by an AI agent. They care that it correctly identifies fish.

Businesses that do not work as autonomous operations also share characteristics: high unit price, custom deliverables, long sales cycles, relationship-dependent trust, and ambiguous success criteria. Enterprise sales. Strategic consulting. Complex B2B services. Healthcare. Legal services. Financial advisory. These are businesses where who is delivering the work matters as much as the work itself. The human is part of the product.

The middle ground, businesses with moderate complexity and moderate price points, is where the most interesting competition will happen over the next two years. These are businesses where an autonomous agent can handle 70-80% of the work, but a human is still needed for the remaining 20-30%. Think of a design agency where the agent produces initial concepts, handles client communications for routine projects, and manages project timelines, but a human creative director reviews final deliverables and manages key accounts. The business is not fully autonomous, but its economics look nothing like a traditional agency because 80% of the labor cost has been removed.

What this means for everyone else

If you are building a business that competes in any of the categories where autonomous agents work well, you should be concerned. The cost structure of an autonomous agent business is so fundamentally different that competing on price is a losing proposition. You cannot match 96% margins on a $99 product when you have employees, office space, and benefits. The competitive response has to be differentiation on quality, trust, or service dimensions that autonomous agents cannot replicate.

If you are running a GTM team, the immediate implication is not that your team will be replaced by an autonomous agent. The implication is that your competitive field now includes entities that can produce and ship products at 10-50x your speed and 1/100th your cost. That changes how you think about market windows, pricing strategy, and what “fast enough” means.

If you are an investor, the portfolio math is changing. The best autonomous agent businesses will not look like traditional startups. They will not need large teams. They will not burn cash. They will be profitable from day one, because their cost structure is fundamentally API calls plus a small amount of human oversight. Evaluating these businesses requires new frameworks. Revenue per employee is meaningless when there are no employees.

We are still early. The agents shipping 85 apps per weekend are impressive, but they are building in categories where “good enough” is the bar. The products that define industries, the ones that change how people work and live, still require human vision and judgment. That will not always be true. The capabilities of these systems are improving on a timeline measured in months, not years. The agent that builds generic utility apps today will build sophisticated SaaS products by next year.

The question for every operator is not whether autonomous agent businesses are real. They are. The question is how long you have before one enters your market. And based on what I am seeing, the answer is: less time than you think.

Enjoying this essay?

Written by

Elom

GTM, growth, and revenue systems operator with 12 years across Fortune 500s, fintech, and B2B startups. Building at the intersection of AI, data, demand, and revenue.

Get the next deep-dive in your inbox

Essays on demand creation, GTM, growth engineering, and revenue systems. Free.